The ‘can’t pay, won’t pay’ conundrum – it doesn’t have to be like this

Published: Jul 8, 2026

Debt

Have you read the ‘Can’t pay, won’t pay’ article from Utility Week recently? It shares the key problems Head of Collections and Collections Managers at energy and water companies are currently facing. And it’s such a perfect example of where digital wellbeing checks can give the extra level of data collections teams need to reach their targets and collect debt safely and responsibly.

The key problems identified by representatives from water and energy companies are:

- Customers don’t want to talk to their supplier

- Suppliers lack proper data so they are missing opportunities to safely collect debt

- The PSR is not a good indicator of financial vulnerability

You can read the Utility Week article here. Read on below for the solutions, because it really doesn’t have to be like this.

Problem: Customers don’t want to talk to you.

Experts quoted in the article state “We’re not good at distinguishing between customers who can’t pay and won’t pay because customers don’t want to talk to us.” and “If you look at our millions of customers and the percentage that contact us per year verbally, it is probably a single digit number.”

Solution: Don’t ask them to talk to you, offer them a safe third-party space to disclose with an obvious benefit.

Customers are 5 x more likely to disclose digitally and to a third party, particularly a trusted B Corp like TellJO, where they’ll get signposts to free tailored support. You can see some of the psychology behind this here, but in short with tools like a digital wellbeing check users experience a reduce fear of judgement, greater control – they can choose when to complete it, and can simply stop if they need to again without judgement (interestingly over 90% who start a wellbeing check, go on to complete it), they can pause and research or translate something and then come back, again something that’s not possible in person or on a phone call.

It works – we’ve re-engaged up to 30% of hard-to-reach customers for utilities. Customers receive personalised signposts to support after their wellbeing check and utilities receive self-disclosed customer data to understand the best next steps.

Problem: Without proper data suppliers are having to be overly cautious chasing debt.

In the article suppliers question whether involuntary pre-payment or litigation is more harmful and also that the simple check box nature of the PSR makes it difficult to make informed decisions. They state “vulnerability is a prime example of where you wouldn’t want to litigate and cause distress to somebody who has mental health problems. Today, mental health is a descriptor on the Priority Services Register (PSR), but you can’t distinguish between mild anxiety and crippling depression.”

Solution: Use digital wellbeing checks to understand the specific mental health conditions customers are facing, so you can tailor collections messages and actions effectively.

We’ve already done this exact project with an energy company. They wanted to know specifically which mental health problems their customers were facing, so they could create dedicated customer care teams who were trained in those key conditions – the results were an extra 150,000 lines of customer data added to their PSR, an additional £800,000 of debt was moved from pay on receipt of bill to direct debit – giving 1900% ROI.

Problem: The PSR is not a good indicator of financial vulnerability.

In the original article “They agree that the PSR is not a good indicator of financial vulnerability. “You may have a medical reliance on electricity, but millions in the bank. It doesn’t impact your ability to pay” and it’s suggested that blanket rules to not chase anyone on the PSR for debt is counterproductive. Similarly efforts to gain access to financial data via financial services and the government are often difficult to progress.

One head of collections at a water company said “Having better access to financial data to identify people who are struggling would help, he says. “It might be that they are increasing their overdraft, or perhaps a few payments have bounced; that kind of information is really gold dust to us.”

Solution: Digital wellbeing checks can give the extra layer of data needed to understand a customer’s financial situation without the need for complex data sharing partnerships.

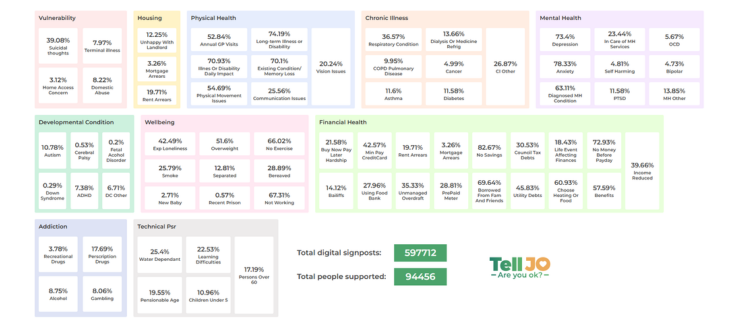

Data sharing can be difficult to set up and can be met with mistrust from customers. With digital wellbeing checks the information is provided directly by the customer. TellJO asks customers clearly at the start of the wellbeing check if they consent to their responses being shared with their utility supplier, over 90% consent, as the wellbeing check messaging is one of support (importantly even if they click no, the customer will still receive their personalised support signposts from TellJO). You can see on TellJO’s wellbeing index the kind of data you can collect from customers including: those experiencing Buy Now Pay Later hardship, those with Council Tax debts, those making minimum payments on their credit card, those choosing between heating or food and those using or have recently used an unmanaged overdraft. See the image below and the live data here for the full picture.

You can also cross reference the data to pinpoint groups of customers and make informed decisions about collections journeys. For example using the scenario given by the original article above, you can identify those who may be medically dependent but not financially vulnerable. You can also see where collections activity risks causing greater harm, for example those with specific mental or physical health conditions who are already financially vulnerable. This is valuable both from a collections perspective but also to know which customers and customer groups would benefit from extra support from your vulnerability or customer care team.

This can be a win-win scenario for collections teams and customers

The advantage of a digital wellbeing check is that it benefits both customers and collections teams. Customers get personalised signposts to support services, the option to receive specific support from their supplier and the chance to share their situation easily and privately, without fear of judgment. Collections teams get the vital information they need to increase payment arrangements without harm to vulnerable customers and without risk to regulation compliance.

If these problems resonate for you, see where digital wellbeing checks can fill your data gaps on a 30 minute call – request a call here.