Digital Wellbeing Checks

Definition: What is a digital wellbeing check?

A digital wellbeing check starts with a simple “are you okay?” and is a series of yes/no questions that helps organisations identify customers experiencing financial hardship, mental health challenges, or other vulnerabilities that may affect their ability to manage bills or services. Customers receive personalised signposts to support following a wellbeing check and organisations can tailor service and support initiatives for maximum impact.

Why Wellbeing Checks Matter

Digital wellbeing checks matter because they help organisations identify customers experiencing financial hardship and vulnerability earlier. By enabling private, structured disclosure, they reveal hidden needs, support early intervention, reduce customer debt and arrears, and allow organisations to provide more appropriate, compliant, and effective support at scale.

Customers are facing increasing financial pressures, rising cost-of-living including food, energy and rent prices has been coupled with rising arrears, particularly in the utilities sectors with levels of customer debt breaking records in recent years.

Financial pressures often come hand-in-hand with mental health struggles, and also the physical symptoms associated with stress. Traditionally debt advice and mental health advice have been separate, making it harder for customers to improve their situation because treating only one element won’t solve the whole problem.

Dr. Thomas Richardson, Clinical Psychologist and TellJO Senior Advisor said:

“Services are largely set up as separate. You go here for your mental health, you go here for your finances. This separation makes it very hard for people to access support. If you are very depressed, being told by a health professional to take a flyer about debt advice might not do a lot. In fact, trials testing just this have been abandoned due to hardly anyone contacting for debt advice in this way. People fall through the gaps between services. But mental health and poverty are so interlinked and overlapping as to essentially be the same problem. To help people with both, we need interventions which tackle them at the same time.”

Digital wellbeing checks bring financial and mental health support services together, signposting a customer to the services needed to improve their situation holistically.

For companies, vulnerability identification is often difficult, relying on customer self-disclosure is likely to miss a significant portion of vulnerable customers (reasons discussed in the sections below). Missed opportunities for disclosure can worsen customer outcomes, turn missed payments into arrears, and increase recovery costs.

Digital wellbeing checks enable organisations to shift from reactive support to proactive support:

- Identify and support customers earlier

- Understand the root causes of financial difficulty

- Provide support before debt becomes unmanageable

- Generate positive brand reputation for customer support

- Comply with regulations on vulnerable customer support – particularly in the finance and utility sectors.

Types of Customer Vulnerability

Vulnerability can be fluid and complex, people move in and out depending on physical and mental health, personal circumstances and life events.

Types of vulnerability can include:

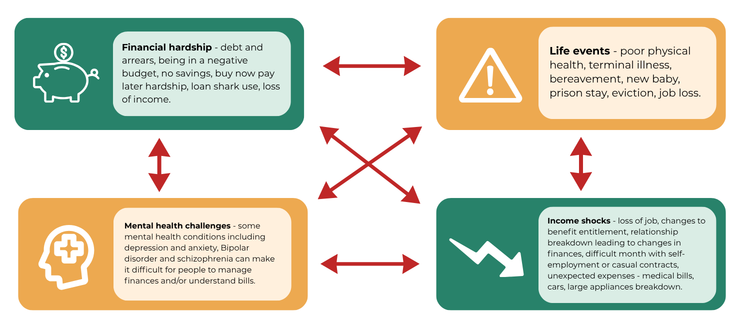

- financial hardship – this could be through debt and arrears, cost-of-living rises or being in a negative budget for example.

- mental health challenges – research has shown that certain mental health challenges can make it harder for a customer to manage their finances and/or to understand bills or pricing to make sure they are getting the best deal.

- life events – unexpected life events can include temporary or prolonged illness, bereavement, a new baby, prison stay, or a Section 21 no-fault eviction (though these are banned as of May 2026).

- income shocks – similar to life events these can include loss of job, changes to benefit entitlement or relationship breakdown leading to changes in finances.

While we’ve categorised some types of vulnerability above, ultimately vulnerabilities don’t happen in a silo. A life event like a sudden but prolonged illness will often come with an income shock due to reduced working or loss of job, leading to financial hardship and mental health challenges associated with both the illness and financial stress. Or someone struggling with gambling addiction may experience financial hardship, mental health challenges and other income shocks like possible relationship breakdown, or new physical symptoms associated with stress. TellJO has found that the average customer qualifying for a utility Priority Services Register has 7.1 vulnerabilities.

Financial hardship and mental health are particularly linked, according to Money and Mental Health Policy Institute research half (46%) of people in problem debt also have a mental health problem.

The image below shows how types of vulnerability can be interlinked:

Not to mention, that despite 45% of the population now being classed as vulnerable according to the FCA definition, only 27% would class themselves as vulnerable. So how do you go about supporting customers who are in debt or difficulty, but don’t consider themselves vulnerable?

Simple. Don’t ask them if they’re vulnerable.

Ask them “are you okay?”

Why Customers Disclose More Digitally

Customers are five times more likely to disclose digitally and to a third party than in person or over a phone call. Why? Behavioural science.

If your energy provider called you up and said “Good morning, tell me about your current mental health and how it’s affecting your ability to pay the bills” is that a conversation you’d feel comfortable having? Probably not.

Here’s the main principles behind why customers disclose more digitally.

- Digitally users experience reduced fear of judgement and less risk of embarrassment or rejection than when speaking to another person.

- There’s greater control with digital channels as users can control what, when and how much they share, they can also easily stop at any time, again without judgement and with greater perceived anonymity than hanging up a phone call.

- Digital channels can reduce perceived power dynamics – for example talking to a representative of a company you owe money to can feel incredibly intimidating, communication or language barriers can also feel like a power imbalance to the person struggling to understand.

- Using digital channels users can control speed and understanding with the ability to pause, research or translate something and then come back. This is particularly useful for people with certain neurodiversities or communication and language barriers.

Many of these principles form part of ‘benign disinhibition’ in the Online Disinhibition Effect, coined by professor of psychology John Suler in 2004, which explored why some people express themselves more freely online. While customers are more likely to disclose vulnerabilities digitally, there will be some who are happy to talk over the phone or self-disclose – these are the motivated few. Often we hear from organisations who have customers self-disclosing and they assume this means they haven’t got a disclosure problem. But if the FCA are saying 45% of the population can be classed as vulnerable, and your organisation’s rates are well under this, it’s likely disclosure is being missed.

Why do customers disclose to TellJO specifically?

As a B Corp certified company and a third party (separate to the company a customer owes money to or receives a service from), several of the principles above can become even more compelling. Telling a company that specialises in supporting those struggling with finances or mental health comes with less risk of judgement and rejection and reduced power dynamic – principles 1 and 3. The customer also has a clear option during the wellbeing check to keep their data private or to share it with the company, giving even greater control – principle 2.

Want more tips for creating a winning disclosure environment? Read this blog post.

How Wellbeing Checks Reduce Arrears

Wellbeing Checks bring together early identification and personalised support to help organisations reduce customer arrears and increase payment arrangements.

By asking the customer if they are okay, a wellbeing check can re-engage 33% of disengaged customers, including those in payment difficulty who may have been avoiding calls or letters, and up to 89% will opt for a payment plan.

Early identification

Digital wellbeing checks can be used at any stage of the customer journey, it could be at first sign of a missed payment or even earlier based on changes in usage or spending patterns, self-disconnection, or other other signs that the customer could be experiencing difficulties or vulnerability. The earlier vulnerability is identified the more likely an organisation can support a customer with the right tariff or signposts before debt and arrears become entrenched.

Where traditional collections fail

Traditional collections methods send a letter, a text message, or call a customer and say, “You have missed a payment. You owe this amount now and you need to pay, if you don’t pay, this is what will happen”. Somewhere in the letter or message will be a link to debt advice or other support. If it’s a phone call, there may be a pause or questions for some self-disclosure.

But even when digital channels are used does this create the right environment for disclosure? For a customer it’s stressful enough experiencing debt or another vulnerability, without receiving multiple chasing letters, messages and calls. If a solution is simply a self-help link like “If you are struggling – tell us here, or get debt advice here”. At what point does the customer experiencing multiple vulnerabilities, get a wave of positive motivation to make this life changing self-intervention? Often it’s not until it’s too late….

Why wellbeing checks work

Instead of focusing on the money owed. Digital wellbeing checks simply ask the customer “Are you okay?” and offer them personalised signposts to support. Based on their answers a digital wellbeing check provides the customer with direct links to relevant support services such as the National Debtline, Mind, the Samaritans or Macmillan Cancer Care for example. Customers tell us that they feel on average 86% better about their situation after completing a wellbeing check, and 98% are likely to use the signposts given.

Once a customer has shared their situation, and understands there is support available we can start to build trust, offer the right support and an affordable payment arrangement. This restores a sense of control for the customer, that they are back in control of their debt and no longer hiding from it or the organisation they owe money to. Deeper understanding of a customer’s vulnerability also allows the organisation to act with humanity, flexibility and empathy towards customers. This creates stronger customer relationships and builds resilience for both the company and the customer.

How wellbeing checks improve customer outcomes

As well as reducing debt, digital wellbeing checks can maximise customer outcomes. Many organisations record vulnerability with a simple yes/no flag, but the key to improving customer outcomes is to ensure support is targeted successfully. To do this, organisations need specific data on what vulnerabilities customers are facing.

TellJO’s Wellbeing Index shows the data that digital wellbeing checks provide, it includes things like percent of customers using a food bank, percent who have recently experienced a bereavement, percent who have been diagnosed with a terminal illness. Understanding any trends among customer groups is the first step to improving outcomes.

How to use digital wellbeing check data to improve customer outcomes:

- Create specialist customer teams trained in the key vulnerabilities customers are experiencing, this could be a team for customers with long-term or terminal illness, specialists trained in supporting customers experiencing domestic abuse or specific mental health conditions.

- Introduce grants or discounts for those who need it – for example if you can see that a large portion of single parent households are in arrears, there’s a gap for targeted support.

- Offer access to financial education and support with benefits and income and expenditure, for those experiencing buy now pay later hardship, unmanaged overdrafts, and other financial hardship, incentivised with matched arrears repayments or similar for those who complete it.

- Partner with or fundraise for specific organisations that can make a difference to customers. This could be food banks, local addiction support groups or community groups to combat loneliness.

- With customers in debt, offer flexible repayment options tailored to their support needs.

How Organisations Use Wellbeing Checks

Digital wellbeing checks can be used in a variety of ways by different industries. Typically either the vulnerability/wellbeing team or the debt team within an organisation will lead on using wellbeing checks, with communication required between the teams to ensure the best outcomes for customers.

Utilities

Digital wellbeing checks have generated a huge return on investment of 1900% for both water and energy companies, while supplying customers with personalised signposts to financial, physical and mental health support. E.ON Next used wellbeing checks to support customers in the ‘mental health’ category on their Priority Services Register (PSR), using digital wellbeing checks to discover the specific mental health concerns their customers were struggling with, then creating dedicated support teams trained in these key concerns. Digital wellbeing checks helped them receive an extra 150,000 lines of data for their PSR. They also sent wellbeing checks to customers who had been in entrenched debt, with no payment plans in place and were able to move over £800,000 of debt from pay on receipt of bill to direct debit. You can read the full case study for E.ON Next here.

Councils

Councils have used digital wellbeing checks in a number of ways: to support residents in Council Tax arrears, to refer residents to their social prescribing teams and to data share with water providers to help more residents benefit from social tariffs. Through a partnership with Adur and Worthing Council and Southern Water, to send digital wellbeing checks to 5,000 residents in receipt of Council Tax Support, TellJO was able to generate 198 positive outcomes for customers (these included bill discounts, capped bills for medical conditions, matched debt repayments) and save these customers £16,177 collectively.

Councils have also used targeted digital wellbeing checks to support residents who they identified as possibly experiencing vulnerability, these included residents who completed a Housing Advice Form, residents in rent arrears, residents in council tax arrears and residents referred for social prescribing support through their GP.

In 2024 and 2025 digital wellbeing checks helped Adur and Worthing Council residents access £146,610 financial support and 258 food vouchers worth £6,425. Read the full case study.

Housing Associations

RHA Wales (now part of Beacon Housing) used digital wellbeing checks to identify which of their tenants were experiencing vulnerability. Digital wellbeing checks saved them an estimated 6-8 support visits per tenant as tenants were more comfortable disclosing digitally. They used this to track trends and ensure they were prioritising their resources for maximum impact for tenants. Read the full case study.

Financial Services

Financial services have a lot of useful MI (management information), but as discussed earlier, customers don’t want to tell their bank they are struggling for fear of negative repercussions. Third party digital wellbeing checks can be used to support customers strategically based on triggers such as mortgage or loan arrears, unusual spending patterns, prolonged minimum credit card repayments, regular unmanaged overdraft use, regular transactions with gambling websites or sudden reductions in income. For the financial services sector, who regularly remind customers not to click links in messages due to fraud concerns, digital wellbeing checks can be offered via nudges through a banking app.

Debt Collection Agencies (DCAs)

Where customer debt has already been passed to a collection agency, digital wellbeing checks can still make a difference to both customer wellbeing and repayment rates. One of TellJO’s DCA clients send a separate digital wellbeing check after the legally mandated initial notification, this allows them to give the customer space to disclose their situation to a third party (see reasons for why customers disclose more digitally above) and make informed decisions on how to collect the debt in a way that leads with empathy and responds to individual needs. The overwhelmingly positive feedback they receive from customers in debt to them proves this makes a big difference to customer wellbeing as well as repayment rates.

Regulation compliance

Sectors are increasingly including the identification and support of vulnerable customers in their regulations. Digital wellbeing checks comply with:

- The Financial Conduct Authority (FCA) Consumer Duty regulations.

- Ogem’s Standard License Conditions (SLCs) relating to vulnerability which are SLC 0, SLC 26 and SLC 27, as well as their Consumer Vulnerability Strategy.

- Ofwat’s Service for all vulnerability guidance, part of the guidance for condition G, specifically G3.5 and G3.6 of the license condition. The Service for all guidance sets out 5 key objectives and 17 minimum expectations, digital wellbeing checks can help water companies comply with 14 of these minimum expectations. For more information on how wellbeing checks can help with Ofwat guidance see this blog post.

FAQs

How do digital wellbeing checks identify vulnerability?

Digital wellbeing checks use a series of mostly yes/no questions and 63 indicators of vulnerability to identify financial hardship and mental and physical health concerns. See how TellJO’s digital wellbeing checks work here.

What does self-disclosure mean?

Self-disclosure is when a person, in this case a customer, chooses to tell a company that they are struggling and need support.

Do you need to have a customer’s phone number to send a digital wellbeing check?

A phone number is ideal, but digital wellbeing checks can also be sent via email, or embedded into a company’s app.

How do digital wellbeing checks keep customer data safe?

TellJO takes privacy and data security very seriously. Information shared by those who take a digital wellbeing check will be stored only if the customer gives us specific consent to do so. Data is only stored for the specific purposes detailed during the wellbeing check and in the Privacy Policy. Data is stored and managed securely to ISO27001:2022 standards and in compliance with data protection laws. Read the full privacy policy.

What is a Priority Services Register?

A Priority Services Register (PSR) is a free to join register held by energy, gas and water companies. It helps them tailor support to households who need extra help with things like bills and meter readings. It’s also used by companies in event of a power cut or water supply issues to ensure customers receive the correct support, for example customers who rely on power for medical machinery, or customers with young children who rely on safe water. Currently each company holds their own PSR, though some data sharing does take place between energy and water companies. Find out more about the PSR.